Dr. Esperanza Buitrago Diaz • Mr. Juan Rafael Bravo

I.1 Corporate Income Tax at Domestic level

Corporate taxes in Colombia are imposed at the national and local levels. Nowadays the term corporate taxation in Colombia includes the income tax, wealth tax, and the trade tax. A solidarity income tax (CREE) was also in force from 2013 until 2016. Given the scope of this work, our report only covers the Corporate Income Tax (CIT). At the end of the work readers find a table with the main features of other taxes. In Colombia, the CIT includes all kind of taxes whose calculation is based on income, capital gains as well as business profits for branches of foreign corporations and entities (article 5 Tax Statute, hereinafter TS[2]).

I.1.1. Active Income

I.1.1.1. Business Profits

CIT is imposed on domestic and foreign corporations. However, whilst Colombian corporations are taxed on their worldwide income, foreign corporations and legal entities (branches and PEs) are taxed only on income and occasional gains of Colombian sources as defined by the TS, mainly (but not limited to): 1) Profits derived by Colombian companies; 2) the transfer or exploitation of tangible and intangible property located in Colombia; 3) the transfer of goods produced in the country, regardless of the place of transfer; the rendering of services in Colombia; 4) the rendering of technical assistance and consulting services, as well as the execution of turnkey contracts, within or outside Colombia (for an extensive list, see 1.2 below).

For residents, the concept and scope of the source rules determine the deductibility of foreign expenses and tax credits.

I.1.1.1.1. Taxable Event

The CIT taxable event is the reception of ordinary and extraordinary income derived in the taxable year that is likely to produce a net increase in equity (patrimony), at the time of their perception. For occasional gains, the taxable event is the windfall of revenues.

I.1.1.1.2. Taxable Basis

The taxable income is determined considering the sum of all ordinary and extraordinary income made in the taxable year that: 1) are likely to produce a net increase in equity at the time of realization, 2) have not been expressly excluded. To calculate the taxable income it is necessary to subtract from the gross income the returns, rebates, ordinary costs incurred in the generation of net income as well as all deductions allowed. Expenses deemed necessary for obtaining taxable income may be deducted if the general conditions for deductibility are met. Taxpayers may deduct the expenses in which they incurred abroad provided that: 1) the expense is necessary (has a causal relationship to income from Colombian sources), 2) the withholding tax was made whenever the payment is taxable income in Colombia for its beneficiary and, 3) there is proof of the withholding (Articles 121, 122 TS). Registration of the contract before the Ministry of Commerce, Industry and Tourism is not required for withholding tax purposes. The Tax Administration (DIAN) considers it mandatory, however.

TS Article |

Deductions |

Income Tax |

107 |

Necessary expenses |

X |

108 |

Wages only when para fiscal contributions have been paid. |

X |

108-1 |

Payments to widows and orphans from armed forces members killed in combat, kidnapped or missing |

X |

108-3 |

Card handling fees |

X |

109 |

Severance paid |

X |

110 |

Consolidated severance |

X |

111 |

Retirement and disability pensions |

X |

112 |

Provision for the payment of future pensions. |

X |

114 |

Contributions to the Colombian Family Welfare Institute, National Learning Service (SENA) and family subsidy |

X |

115 |

Paid Taxes. 100% of the Industry and Commerce Tax and property tax. 50% of the financial transactions tax |

X |

116 |

Taxes, royalties and contributions paid by decentralized bodies |

X |

117 |

Interest |

X |

118 |

The inflationary component of interests is not deductible |

X |

119 |

Interest on loans for house purchase |

X |

120 |

Adjustments for exchange differences |

X |

121 |

Expenses abroad |

X |

122 |

Limitation of cost and deductions |

X |

124 |

Payment to the head office |

X |

124-1 |

Other non-deductible payments |

X |

124-2 |

Payments to tax heavens |

X |

125 |

Donations |

X |

126 |

Contributions to mutual funds |

X |

126-1 |

Contributions to disability and retirement pension funds and unemployment funds. |

X |

126-2 |

Donations to foundations and corporations dedicated to the defense, protection and promotion of human rights and access to justice |

X |

126-5 |

Donations for natural parks and natural forests |

X |

127-1 |

Leasing contracts |

X |

128 |

Depreciations |

X |

129 |

Obsolescence in depreciable assets |

X |

142 |

Amortization of investments |

X |

145 |

Provision for doubtful or difficult collection debts |

X |

146 |

Manifestly lost or worthless debts |

X |

147 |

Compensation of tax losses of companies |

X |

148 |

Loss of assets due to force majeure |

X |

149 |

losses on alienation of assets |

X |

151 |

Non-deductibility for losses in sales of assets to related parties |

X |

152 |

Non-deductibility for losses in sales of assets from a company to their shareholders |

X |

153 |

Non-deductibility for losses in sales of shares and contributions |

X |

154 y 155 |

Non-deductibility of bonds |

X |

157 |

New investments in plantations, irrigation, wells and silos |

X |

158 |

Amortization in the agricultural sector |

X |

158-1 |

Investments in scientific and technological development |

X |

158-2 |

Investments in control and improvement of the environment |

X |

159 |

Investments in the oil industry and mining sector. |

X |

160 |

Hydrocarbons exploration in contracts in existence at 28 of October 1974 |

X |

161 |

Exhaustion of exploitation of hydrocarbons in contracts in existence at 28 of October 1974 |

X |

166 |

Special deduction on exploitation of hydrocarbons |

X |

167 |

Exhaustion in exploitation of mines, gases different from hydrocarbons and natural gas deposits |

X |

171 |

amortization of investments in gas and mineral explorations |

X |

173 |

In reforestation plantations |

X |

174 |

Sums paid as annuity |

X |

176 |

For the livestock business |

X |

177 |

Limitation of costs are applicable to deductions |

X |

177-2 |

Common costs and expenses limitations. |

X |

Expenses incurred abroad are deductible if they are associated with getting domestic source income (article 121 TS) and there are limited to 15% of the taxpayer’s net income, calculated before the discount of such costs or deductions (article 122 TS). Some expenses are deductible without restraining to the 15% limit mentioned, e.g. 1) payments subject to withholding tax, 2) short-term loans for the imports of goods and bank overdrafts, 3) appropriations made for financing or pre-financing exports, 4) payments made to brokers located outside Colombia for the purchase of goods or raw material up to certain amount determined by the government, 5) interest paid on short-term loans acquired to finance the import or export of goods if certain requirements are met, 6) payments that are not of Colombian source; 7) expenses related to the reparation and maintenance of equipment abroad, 8) the training of personnel services provided abroad to public entities, 9) payments for the purchase of tangible goods; 10) costs and expenses capitalized for future depreciation, and 11) costs and expenses related to the compliance of legal obligations. Direct or indirect payments made to foreign parent companies or offices for management, royalties and exploitation or purchase of intangibles are deductible as a general rule, provided the corresponding withholding was applied, if mandatory and if such transaction comply with transfer pricing rules.

Nondeductible expenses include dividends, expenses that are deemed not to have a causal relationship with the production of income, income tax and VAT, net worth tax, registration tax, stamp tax and vehicle tax. Payments to related individuals or legal entities located, incorporated or operating in tax havens are deductible as long as the taxpayer (if it is a related party) complies with the documentation indicated in article 260-7-3 TS concerning the transfer pricing regime.

The foreign WHT is creditable against the final income tax liability of Colombian residents if the foreign tax does not exceed the tax which would have been due in Colombia on that income. Income from Colombian sources derived by foreign companies without a permanent presence in Colombia is subject to WHT. If the withholding is applied a tax declaration is not required.

In the determination of the taxable income in Colombia is important to stress that corporations and entities are also expected to establish their taxable income according to an alternative “presumptive income” system. In this case, the minimum taxable income must be equal

to at least 3,5% of the company’s tax equity determined as of 31 December of the immediately preceding calendar year. The income tax applies to the higher of the net income or the presumptive income.

I.1.1.1.3. Taxpayers

Corporate income tax is imposed on:

- Domestic corporations and entities having their effective place of management in Colombian territory in the taxable year or period (irrespective of incorporation abroad, DIAN Concepto 61818 of 2014). As to the law that is the place where the decisive and necessary commercial and management decisions to carry out the activities of the corporation or entity as a whole are taken.

Foreign corporations that have issued stock or bonds in the Colombian stock exchange or in a recognized foreign stock exchange are not considered to have their effective place of management in Colombia. The subsidiaries of such companies are also not considered to have their effective place of management in Colombia to the extent that there is consolidation in the financial statements of the parent. Such subsidiaries can elect to be treated as a national corporation unless they are 80% Foreign Income Companies. - Corporations or entities having their main domicile in Colombian territory,

- Corporations or entities incorporated in Colombia according to Colombian law,

- Permanent establishments (hereinafter PEs) as defined for domestic tax purposes, i.e. a fixed place of business located in Colombia through which a foreign company or a non-resident individual performs all or part of its activities. Colombian tax law provides the following list of examples: branches, agencies, offices, workshops, mines, oil or gas wells, or any other place involving the extraction or exploitation of natural resources. Independent agents and activities of ancillary or preparatory character (as defined by Decree 3026, 2013) are excluded from the scope of the definition. In a number of rulings the Colombian Revenue Service (DIAN) stated cases that do not configure a PE, for instance a foreign portfolio investment (DIAN, Oficio 5468 of 2016). Representative offices of foreign financial institutions whose only purpose is to promote or advertise services do not constitute PEs due to the ancillary and preparatory character of the activities (DIAN, OFICIO N° 029266 of 2014). Permanent Establishments are required to get a tax number, present tax returns and the income taxable in Colombia follows the rules of the force of attraction if the income is deemed to be of Colombian source (Decree 3026, 2013).

- Non-resident companies and entities are subject to CIT depending on whether they perform their activities directly, through a branch or a permanent establishment. If the latter is the case, branches are subject to the same rules as residents but are taxed only on their income from domestic source. Branches of foreign companies that derive income in Colombia must file tax declarations.

- Foreign companies deriving more than 80% of their income (other than passive income) in the jurisdiction of incorporation are not considered to have their effective place of management in Colombia. Article 12, paragraph 5 TS rules the 80% calculation of income generated abroad.

- A special regime (hereinafter CITS) applies to nonprofit organizations meeting certain requirements and as long as they are not excluded by the law.

Enterprise collaboration agreements such as consortiums, joint ventures, unincorporated temporary joint ventures are not subject to the CIT themselves. Instead, each of the parties bear the tax liability.

I.1.1.1.4. Tax rates

The corporate income tax rates vary depending on whether corporations or entities are located in the Colombian Free Trade Zones (FTZ). In the FTZ the CIT is 20%[3](but 15% in Cucuta). Out of the FTZ a 34 or 33% apply, as follows:

Corporate Income Tax Rate |

34% in 2017, 33% as from 2018 |

Corporate Income Tax Surtax |

6% for 2017, 4% for 2018, none in 2019 (on taxable income in excess of 800 million Colombian pesos, hereinafter COP). |

Capital Gains Tax Rate |

10% |

Branch and PE Tax Rate |

34% |

I.1.2. Passive Income

I.1.2.1. Dividends

The taxation of dividends varies depending on whether the dividends are paid between domestic companies, Andean Community companies, or in inbound or outbound situations. Dividends received by a domestic company from another domestic company are not subject to CIT if the distributing company has already paid taxes on the profits distributed. The portion of dividends distributed by an Andean MNE corresponding to profits earned by a branch in another Andean Member State will not be taxed in the country of the headquarters.

From FY 2017 onwards, dividend distribution is taxed; this means that only dividends paid out of profits obtained in FY 2017 should be subject to the dividend tax

I.1.2.1.1. Taxable Event

The concept and taxable event is defined in article 30 of the TS, as any distribution of benefits, in money or in kind, in charge to the company’s equity that is made to partners, shareholders, members, associates, subscribers or similar, except for capital reductions and share placement premiums. It is also defined as any transfer of profits corresponding to occasional gains from national source, from permanent establishments or branches in Colombia from non-resident persons, to related parties abroad.

I.1.2.1.2. Taxable Basis

Amount of dividends distributed to the tax payer.

I.1.2.1.3. Taxpayers

According to articles 48 and 49 TS, dividends are taxed in the hands of the shareholders of Colombian companies.

I.1.2.1.4. Tax rates

This tax is applied regardless of the profits being taxed or not at the distributing company level, and the rates differ depending on the residence of the beneficiary.

For a resident company, dividends are not taxed if profits out of which the dividends are paid, already have been taxed at the corporate level. Dividends out of profits not taxed at the corporate level, are taxed at a rate of 33%.

I.1.2.2. Interest

Income from interests is subject to the general rules of the CIT described before.

I.1.2.2.1. Taxable Event

See section I.1.1.1.1.

I.1.2.2.2. Taxable Basis

I.1.2.2.3. Taxpayers

See section I.1.1.1.3.

I.1.2.2.4. Tax rates

See section I.1.1.1.4.

I.1.2.3. Royalties

Income from royalties is subject to the general rules of the CIT describe before.

I.1.2.3.1. Taxable Event

See section I.1.1.1.1.

I.1.2.3.2. Taxable Basis

See section I.1.1.1.2.

I.1.2.3.3. Taxpayers

See section I.1.1.1.3.

I.1.2.3.4. Tax rates

See section I.1.1.1.4.

I.1.3. Special Features of the CIT system

I.1.3.1. Existence of Group Regime

Colombian tax law does not have a group regime.

I.1.3.2. Treatment of Losses

Losses may be offset against the income generated in the following 12 years, unless they relate to: 1) Losses related to proceeds that are not considered income or occasional gains, 2) costs or deductions not related to the generation of taxable income. Tax losses generated until 2016 could be carried forward without time limitation. Carryback is not possible.

Losses not deductible include: 1) losses related to the alienation of assets to related parties; 2) losses related to the alienation of assets whenever the transaction takes place between the limited company or assimilated company and its partners (provided they are individuals or not settled successions, the spouse, relatives of the partners within the fourth degree of consanguinity and the second of affinity or only civil one; 3) losses related to the alienation of shares or quotas of social interest and 4) loses related to the alienation of special financial bonds;

I.1.3.3. Tax Holidays

Tax holidays related to the CIT include mainly the regime applicable in the Free Trade Zones (FTZ), reduction of statutory CIT rates, exemptions, tax free mergers and demergers, and a special tax credit on payroll payments.

I.1.3.3.1. Free Trade Zones

Industrial enterprises located at the FTZ enjoy a 20% CIT on income derived from the FTZ operations. By exception Cucuta has a 15% CIT rate. Capital Gains are taxed at a rate of 10%. For commercial users apply a 34% CIT and as from 2017 the CIT is 33%.

I.1.3.3.2. Reduced statutory CIT rate for SMEs

SMEs within certain brackets are subject to a reduced CIT rate of about 9% for five years applicable either from the moment they started their operation, or from the moment in which they obtain taxable income.

I.1.3.3.3. Exemptions of the CIT

As from 2018 income exempted from CIT includes: 1) income exempt under AC Directive 578, 2) funds of the pension system, 3) amounts due, interests, commissions and other financial interest due by official entities of financial character as well as of cooperation entities ,for the development from countries to which Colombia has signed cooperation agreements, 4) income from the use of foreign plantations, investments in new sawmill related to the new plantation, 5) income from donations or aid to entities to foreign governments, 6) Income from the sale of electric power generated from wind, biomass, or agricultural waste, for a period of 15 years, as long as a) the seller issues and negotiates Greenhouse Gas Reduction Certificates in accordance with Kyoto’s Protocol and b) 50% of the income obtained in the sale of the certificates is invested in social projects of the region in which the generator operates, 7) income related to social housing or priority interest according to the conditions set by law, 8) Income obtained from hotel services offered in new hotels built within 15 years counted from 2017. This exemption is available for a term of 30 years.

The following tax exemptions of the CIT are only available up to 2017: 1) income from river transport services with shallow drafts, 2) Income obtained from hotel services offered in refurbished or enlarged hotel facilities, provided that certain conditions are met. 3) Leasing agreements with option to purchase real state built for sale, 4) Income obtained from ecotourism services, 5) a kind of patent box consisting or an exemption of income derived from new medicinal and software products developed in Colombia and patented in Colombia.

I.1.3.3.4. No taxation of mergers and demergers

Mergers and demergers are free of tax provided that the following conditions are met: 1) the surviving entity or the beneficiary entity is a resident, 2) de-mergers are over units of business/going concern (substance requirement), 3) the value of the shares received by shareholders owning at least 75% (85% for related parties) is proportional to the one prior to the merger or de-merger., 4) the shareholders receive at least 90% of value in shares (99% if participants are related), 5) The income tax due for the sale is increased on a 30% whenever the shareholders sell the shares received within two years of the merger/de-merger. The above mentioned also apply if the participants are not residents if the assets held in Colombia represent 20% or less of the worldwide aggregate of assets of the group.

I.1.3.3.5. Tax credit on payroll payments

Employers hiring any of the following persons benefit from a tax credit: 1) individuals below 28 years old, 2) women above 40 years old provided that they have not been legally employed in the previous year; 3) workers earning less than 1.5 times the minimum monthly wage (around COP 1,106,576); 4) disabled persons, persons reintegrated to democracy (from the military conflict), or displaced persons as consequence of the internal conflict in the conditions stated by the law.

I.1.3.3.6. Special new investments

- New investments in environmental preservation control and enhancements are subject to a 25% deduction provided that certain conditions are met. (article 255 TS)

- Full deductions for qualified research and technology development projects if certain conditions are met.

Other deductions are indicated in I.1.1.1.2.

I.2. Corporate Income Tax on International Level

Considering that resident corporations and entities are subject to income tax on their worldwide income whilst non-resident companies, including their local branches, are only taxed on their Colombian-source income, the concepts of residence and source play an important role at the international level.

Non-residents are taxed depending on whether they perform their activities directly, through a branch or a permanent establishment. If the latter is the case, branches are subject to the same rules as residents but are taxed only on their income from domestic source. Branches of foreign companies that derive income in Colombia must file tax declarations. Permanent Establishments are required to get a tax number, to keep accounting books, and to submit tax returns. PE’s taxable income in Colombia follows the force of attraction rule if the income is deemed to be of Colombian source (Decree 1625, 2016). For purposes of attribution of profits to the PE it is necessary to have a study of functions, assets, risks and personal involved in the generation of income or perception of gains. Whenever the head office performs activities in Colombia that are not attributable to its branch or PE, the proceeds not attributable are subject to a withholding tax of 33%.

The TS defines PE´s for domestic purposes as a fixed place of business located in Colombia through which a foreign company or a non-resident individual performs all or part of its activities. The following are included in the exemplificative list: branches, agencies, offices, workshops, mines, oil or gas wells, or any other place involving the extraction or exploitation of natural resources. Independent agents and activities of ancillary or preparatory character as well as representation offices of foreign reinsurance companies are excluded from the scope of the definition. Tax treaties may contain different definitions.

The decisive criteria to determine whether companies and entities are residents for CIT purposes is the place of effective management in Colombian territory during the taxable year or period. Such criteria include 1) the place wherein business and management decisions, which are decisive and necessary to carry out the activities of the company or legal entity as a whole, are made; 2) having their domicile in Colombian territory; and 3) incorporation under Colombian law[4]. In order to establish if there is residence, a factual test applies. Special attention is paid to facts related to the places where senior executives and managers of the company usually exercise their responsibilities and carry out the daily activities of the company’s upper management. If a company has its effective place of management in Colombia it needs to keep a tax number of registration (so called RUT) and accounting records in accordance with the Colombian regime.

Notwithstanding the above, the law establishes that foreign companies won’t be considered residents even if its place of effective management is in Colombia, whenever they: 1) issue bonds or stock in the Colombian stock exchange (Bolsa de Valores) or in a qualified foreign stock exchange according to an administrative ordinance issued by the DIAN. Likewise, in the case of subsidiaries of a parent company that issues bonds or stock as explained above, as long as the subsidiary has its financial statements consolidated with its parent company. A list of stock exchanges that are recognized for applying the exception to the rule of effective place of management for foreign entities is set by Administrative Regulation 57 of 2016 provides; and 2) foreign companies that obtain 80% or more of their income in their country of incorporation. Passive income (like interest and royalties) shall not be considered for determining this percentage. Dividends obtained directly or indirectly will be considered passive income as long as they are derived from direct or indirect participations of 25% or less in the capital of the foreign company.

The concept of source is fundamental and the law indicates the cases in which the income derived is deemed to be of Colombian source. Article 24 TS states, amongst other cases: 1. Transfer or exploitation of tangible and intangible goods located within Colombian territory; 2. Transfer of goods within Colombian territory; 3. Rendering of services within Colombian territory; 4. Rendering of technical services, technical assistance and consulting services, and the undersigning of turn-key contracts, inside and outside Colombia; 5. Earning of profits by Colombian companies; 6. Returns on credits owned in Colombia; 6. The profits from manufacturing or industrial processing of goods or raw materials within the country, irrespective of the place of sale or disposal; 7. Income derived from commercial activities within Colombia; 8. For the contractor of “turnkey” contracts and other contracts for the preparation of material works, the total value of the respective contract; 9. In general terms, foreign source income includes any revenues arising from the transfer or exploitation of tangible and intangible goods located outside of Colombia, and the rendering of services abroad. Furthermore, income generated upon certain foreign loans is not deemed as local source income.

I.2.1. Inbound Transactions

Inbound payments received by Colombian corporations are part of the CIT taxable base in the same manner as income of Colombian sources. Inbound dividends are part of the taxable base from the income tax and CREE and the taxpayer has the right to a tax discount that works as an ordinary tax credit applicable to the CIT (Article 254 TS) and CREE (Article 22-5, Law 1606, 2012).

1.2.1.1 Business profits

Foreign-source income and capital gains obtained by individuals, corporations or assimilated entities through a branch or PE are subject to CIT and surtax (depending on the taxable year CREE may also apply). The attribution of profits takes into account the risks, functions, assets and personnel involved whilst obtaining the income.

1.2.1.2 Inbound dividends

Inbound dividend are included in the general taxable base and treated as ordinary income. A tax credit is available in the terms previously mentioned.

1.2.1.3. Interest, royalties and other income

These types of passive income are included in the general taxable base and follow the same rules of other revenues. A tax credit is available in the terms above mentioned.

I.2.1.4. Capital gains

The capital gains tax is levied on the actual disposal of fixed assets owned for more than 2 years (for lower periods of time such gains are treated as ordinary income), on inheritances, donations, the benefits of the surviving spouse, the liquidation of legal entities that have existed for more than 2 years, and prizes from lotteries, raffles and profits. Special rules apply for the calculation of the capital gains for each of the cases indicated. Capital gains can only be compensated with capital losses. Domestic tax law does not set provisions for a deferral of the capital gains tax.

I.2.2. Outbound Transactions

1.2.1.1 Withholdings applicable

Outbound transactions are subject to withholding taxes if income is from domestic source. The main withholdings applicable to cross border transactions are as follows:

|

General clause Income derived from |

Fee for payments |

||

Exploitation of material and intangible goods |

Within Colombia |

Royalties or exploitation of industrial property or know-how. Profits or royalties derived from literary, artistic or scientific work |

15% of the nominal value of the payment/CA |

Exploitation of cinematographic films |

15% of the gross value of the payment/CA |

||

Exploitation of computer software |

33% on 80% of the payment/CA |

||

Alienation of material or intangible goods |

Located within the country by the time of its alienation |

Occasional gains (art. 415 ITA) Rate for profits or exploitation of industrial or intellectual property (art. 408 ITA) |

10% on the gross value of the payment/CA 15% of the nominal value of the payment/CA |

Licensing services or right to use software |

Inbound payments to Colombian taxpayers subject to IT in Colombia |

Licensing services or right to use software |

3.5% of the payment/CA |

Provision of services |

Within Colombia Permanent or temporary With or without and establishment |

Provision of services and technical assistance Technical services provided by non-resident persons |

15% of the nominal value of the payment |

Turnkey contracts |

When the contractors are foreign companies or entities without domicile in Colombia, natural persons without residence in Colombia or illiquid successions from persons not residing in the country at the time of his death |

1% of the value of the contract |

|

Interest |

15% of the payment |

||

Payments to tax heavens |

When the beneficiary is an individual or any kind of entities created, located or functioning in tax heavens |

33% of the payment (34% in 2017) |

|

Dividends |

Dividends paid to foreign companies or entities without domicile in Colombia. Dividend is attributable to a permanent establishment or branch resident in Colombia from the foreign entity (article 246TS) |

5% if such dividends and participations were taxed at the level of the Company. 38.25% if such dividends were not taxed |

|

Others |

Cases without a specific provision |

15% on the gross value of the payment |

|

I.2.2.2 Business profits

Foreign entities are taxed on the business profits related to operations directly attributable to their Colombian branch or PE on their income from Colombian sources. When the head office performs activities in the country directly, which are different from those attributable to its branch or PE, the head office is subject to withholding tax at a rate of 33%.

Some payments to parent companies are not deductible, for instance 1) interest and other financial expenses unless they comply with the transfer princing rules or are owed to financial entities under the supervision of the Financial Superintendence, 2) payments to residents of low tax or preferential jurisdictions, unless the 33% withholding was applied and there was a transfer pricing analysis. This does not apply to financial transactions registered at the Central Bank, 3) capital losses derived from the transfer of assets between related parties or from the alienation of shares or partnership interests.

The transfer pricing rules apply to transactions between the PE and the head office or related parties.

I.2.2.3 Dividends, interest and royalties

Dividends, interest and royalties earned by non-residents through a Colombian branch are included in the taxable base of the branch and subject to tax at the general rate. The withholding tax and rates on outbound payments are indicated in 1.2.1.1.

I.2.2.4 Special features

I.2.2.4.1. Relief Methods

Under domestic tax law an ordinary tax credit is available for taxes paid abroad provided that the income is of foreign source and the tax does not exceed the amounts applicable in Colombia on the same income. The calculation of the tax credit follows the formula set by article 254 TS. The value of the discount equals the result of multiplying the amount of dividends or participations by the income tax rate on which the utilities that generated those dividends or participations has been subjected abroad, multiplied by the following proportion:

- In the case of the CIT:

- In the case of the CREE

Where

- TRyC is the tax rate of the Income tax applicable to the taxpayer for the foreign source income.

- TCREE is the tax rate of the CREE applicable to the taxpayer for the foreign source income.

- STCREE is the tax rate of the surcharge of the CREE applicable to the taxpayer for the foreign source income.

Considering that as from 2017 the CREE is no longer in force, dividends paid to a resident will be included in the taxable income of the recipient and taxed at a rate of 34% for 2017 and 33% for 2018. The tax credit will be equal to the amount paid abroad but limited to the amount of tax to be paid in Colombia.

I.2.2.4.2. Tax havens

Colombian tax law no longer refers to tax havens. Instead, the law adopted the OECD terminology of non-cooperative, low tax jurisdictions and preferential regimes. The law set a list of criteria for the government to consider whilst issuing the list of non-cooperative jurisdictions: 1) the lack of tax rates or the existence of low income nominal rates compared to the applicable ones in Colombia for similar transactions, 2) the lack of effective exchange of information or the existence of legal rules or administrative practices restraining it, 3) the lack of legal, regulatory or administrative functioning transparency, 4) the absence of substantive local presence, the exercise of a real activity and economic substance and 5) any other criteria internationally accepted to establish whether a jurisdiction is non-cooperative, low or zero tax jurisdiction. In 2013 and 2014 the law issued a list of tax haven jurisdictions. The list can be updated from time to time by the Government. The law presumes a preferential regime whenever two of the criteria listed in numbers 1 to 4 are met, or a jurisdiction offer tax benefits only to non-resident entities or individuals excluding its own residents of the application of the law.

Transactions with residents of the abovementioned jurisdictions are subject to the transfer-pricing regime irrespective of whether the parties are related or not. Hence, taxpayers are requested to file a transfer pricing study and a transfer pricing return for transactions above 10,000 taxable units. If the transactions is between related parties, the taxpayer is required to provide a transfer pricing study including functions performed, assets used and risks assumed, costs and expenses related to the provision of the service from the non-cooperative jurisdiction. Furthermore, a 33% withholding tax applies as from 2018 (34% until 2017), for any payment or proceed that constitutes taxable income.

I.2.2.4.3. Tax Returns for non-residents

Nonresidents are required to file a tax return whenever: 1) the entire income of Colombian sources is not income from dividends, interests, commissions, fees, royalties, compensations for personal services, exploitation of intellectual property (including motion pictures and software), know how, technical assistance, technical services, consultancy, 2) the withholding taxes have not been made for payments of dividends, interest, commissions, fees, royalties, personal services, exploitation of intellectual property, know-how, technical assistance services or technical services, and 3) the alienation of shares or quotas in Colombian companies (in addition to the cancelation of the foreign investment at the Central Bank.

I.3. Anti-Avoidance Legislation

Anti-avoidance provisions in Colombia are evolving. As from 2016 there is a general anti-avoidance clause (Article 364-1 TS), a specific antiabuse provision for nonprofit organizations (article 364-2 TS) and the law set as a crime the failure to include assets or the inclusion of non-existent liabilities (article 434A). Taxpayers that willfully omit assets or submit inaccurate information on such assets or that declare non-existent liabilities up to an amount equal or higher than 7.250 minimum monthly salaries with an impact in its CIT may be imprisoned for about 48 to 108 months and a penalty equivalent to 200% of the value of the asset omitted, of the value of the asset inaccurately declared or of the value of the non-existing liability, unless the taxpayers presents or corrects the tax return or later returns and pay if that were the case.

The new special provision anti abuse states that the CITS neither applies to nonprofit organizations abusing the legal configuration to defraud the tax law applicable, nor to sham transactions or to inexistent business. In these cases, the law allows the Revenue Service to: 1) declare the existence of the abovementioned behaviors, only for tax purposes, without the need of judicial intervention, and 2) to re-characterize and recalculate the taxes due, the default interest and the penalties for inaccuracy. The provision applies irrespective of whether the situation involves taxpayers or non-taxpayers and also presumes that a business structure constitutes abuse, fraud or simulation in the following cases:

The main purpose of the entity is an economic exploitation targeting the direct or indirect distribution of surpluses, instead of serving a general interest through the performance of meritorious activities.

Availability or possibility to access special benefits or conditions to access the goods or services offered by the entity, by the founders, partners, statutory representatives, members of the bodies of direction, spouses or relatives up to the fourth degree of consanguinity of any of them as well as any entity or person with whom any of the aforementioned persons has the status of related economic party in accordance with Articles 260-1 and 450 of the Tax Statute Possibility to access special benefits or conditions to access the goods or services offered by the entity, to

The direct or indirect acquisition of goods or services acquired directly or indirectly by founders, associates, statutory representatives, members of the governing bodies, spouses or relatives up to and including the fourth degree of any of them, as well as any other entity or person with whom any of the aforementioned persons is a related party in the terms of articles 260-1 and 450TS.

The acquisition of the right to participate in the economic results of the entity directly or through person or interposed entity as a consequence of consideration for the work of the founders, associates, statutory representatives and members of the governing body or any employment relationship contracted by the entity.

The perception of allegedly donations, money, goods or services that the nonprofit entity compensates directly or indirectly to the donor. Such amounts will be taxed as income different to the one of the entity’s purpose without possibility to deduct the payments from the CITS.

Before the abovementioned legislation was in force, as well as a GAAR was introduced in 2012, the Constitutional Court in 1996 acknowledged the possibility for the DIAN to apply the “abuse of legal forms” and “legal fraud”, whenever there was any indication that the taxpayer used some legal clothing to reduce its tax burden by keeping the taxable event from occurring and where the transaction itself lacks any economic substance (CC, C – 15 of 1993 and C -540). The Court held that this power of DIAN is based upon the application of the constitutional principles of substance over form (Article 228) and equitable application of taxes (Article 363). Such interpretation of the Colombian Constitutional Court is not binding since it does not have erga omnes effects because it was included in the considerations of the judgments and not in the decision per se. Legally such case could be considered jus an auxiliary criterion for judicial activity (Article 48 of Law 270 of 96 and Article 23 of Regulation 2067 of 1991.

Based on the abovementioned decisions, DIAN issued the Ruling 51,977 of August 2, 2005 instructing tax officials to establish that an abuse of legal forms has taken place in any case of tax evasion or avoidance, re-characterizing the transactions so that the taxable event occurs, and imposing a fine for inaccurate reporting equal to 160% of the related tax deficiency. Now, despite that these types of rulings are binding upon the tax administration, tax advisers felt they were neither binding upon the taxpayers nor upon the tax courts.

I.3.1. Abuse of Law

According to the 2016 Colombian GAAR, article 869TS, the abuse of law for tax purposes regards transactions or series of transactions involving the use or implementation of one or more artificial acts or legal transactions without economic or commercial purpose to obtain a tax advantage irrespective of any subjective intention. The law defines artificiality and tax advantage as follows:

A tax advantage is taken by the alteration, the disfigurement or modification of the tax effects that would otherwise be generated on a taxpayers or beneficial owner, as for instance the elimination, reduction or deferral of the tax, an increase in the credit balance or of the tax losses as well as the extension of tax benefits or exemptions.

Artificiality is presumed whenever 1) the transaction is not sound (reasonable) in economic or commercial terms, 2) the legal act or business results in a high tax benefit not reflected in the economic or business risks assumed by the taxpayer, 3) the substance of an act or transaction hides the true will of the parties.

In the abovementioned circumstances DIAN may re-characterize or reconfigure any transaction or series of transactions by establishing its true nature and ignoring the effects of the artificial ones. Furthermore, DIAN is entitled to issue a new assessment of the taxes, interests and sanctions.

I.3.2. Thin Capitalization Rules

Thin capitalization rules are applicable in Colombia since 2013 (article 118-1 TS). Interest expenses can only be deducted if they are derived from indebtedness and the average value of debt does not exceed three times the entity’s net equity. A ratio 4 to 1 is in place for special purpose companies, entities or vehicles whose purpose is the construction of social housing. The equity taken into account is the taxpayer’s net equity for the preceding year, and the debt taken into account is debt that accrues interest.

Thin cap rules are not applicable to interests generated in credits granted by companies under the surveillance of the Financial Superintendence of Colombia or foreign entities under the surveillance of the authority watching the financial system provided that the Taxpayer meet certain conditions (article 118-1 TS). These, however, neither apply to credits granted by foreign associated enterprises as defined by the transfer pricing regime, nor to credits granted by entities located in non-cooperative jurisdictions (article 118-1 TS).

I.3.3. CFC Legislation

Colombia introduced CFC rules in 2016. CFCs are defined as corporations and investment vehicles –e.g. trusts, collective-investment funds, and private interest foundations-, meeting the conditions to be considered a related party for transfer pricing purposes. The CFC regime applies to residents (including corporations and entities) that directly or indirectly hold an interest equal to, or greater than 10% of the capital or of the profits of a foreign entity considered as a CFC.

According to the CFC rules, taxpayers subject to the CIT should not wait to receive a distribution of profits in Colombia to recognize the net profits of the CFC derived from passive income, in proportion to their participation in the CFC’s capital or profits.

For CFC purposes, the following proceeds are considered as passive income: 1) Dividend and profit distributions from a company or investment vehicle, 2) Interest, 3) Income derived from the exploitation of intangibles, 4) Income from the sale of assets that generates passive income, 5) Income from the sale or lease of immovable property, 6) Income derived from the sale or purchase of tangible goods acquired from (or sold to) a related party if the manufacturing and consumption of the goods occurs in a jurisdiction different from the one in which the CFC is located or is tax resident, 7) Income from the performance of certain services in a jurisdiction different to the one of residence or location of the CFC.

It is important to note that whenever the dividends and benefits distributed by a CFC have been already taxed in Colombia, the income should be considered non-taxable for the Colombian taxpayer.

A tax credit is allowed for taxes paid abroad with respect to the passive income whenever the Colombian tax resident recognizes taxable income under the application of the CFC rules.

I.4. Tax Treaty Law

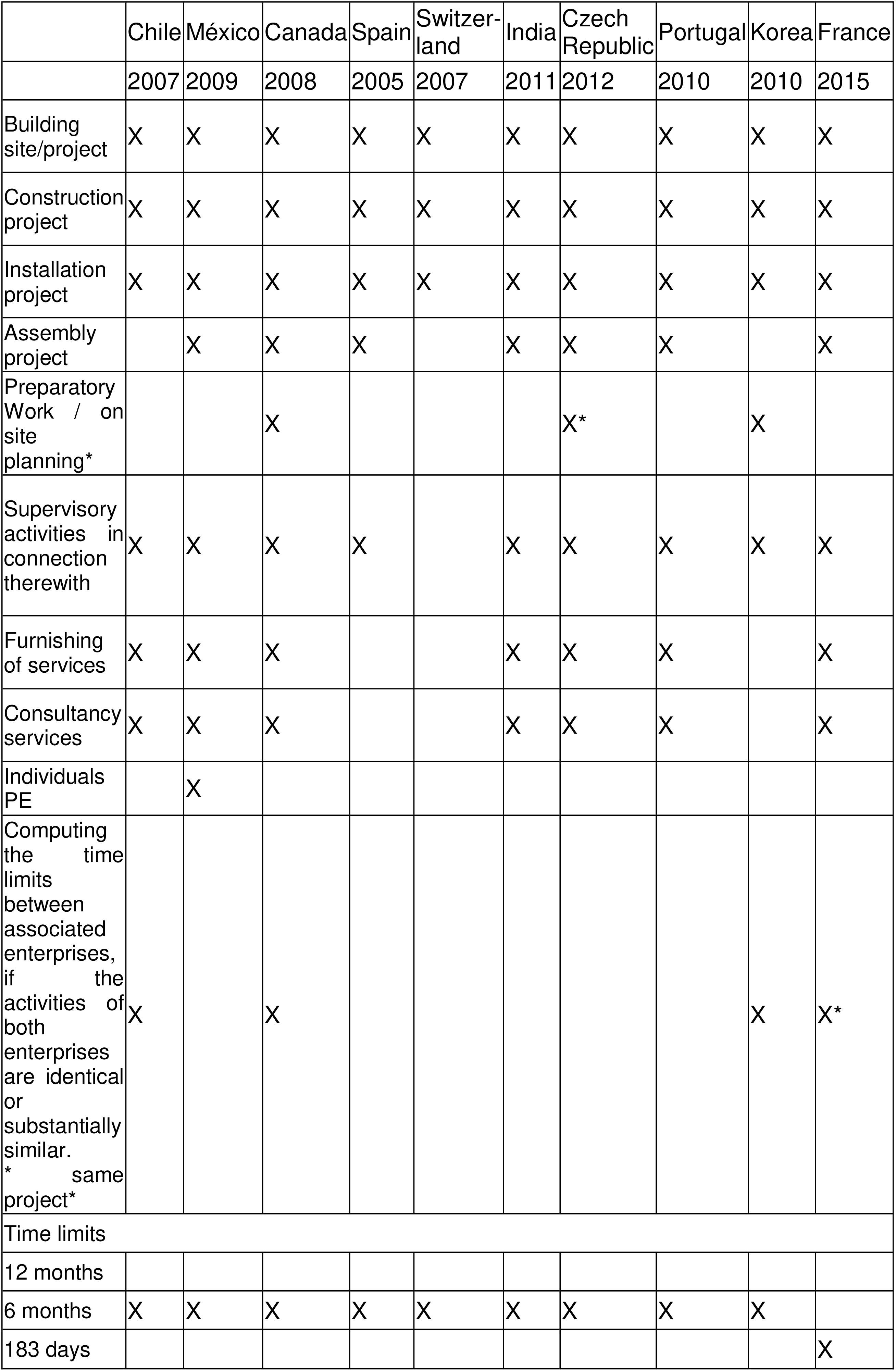

Colombia started negotiating Conventions for the Avoidance of Double Taxation in the seventies. At that time treaties were related to income for shipping and air companies and were negotiated with Germany, Argentina, Brazil, France, Italy, Panamá, Venezuela and the United States of America. The negotiation of Double Taxation Conventions on Income (DTC) started in 2005 with the tax treaty with Spain. Thenafter other treaties negotiated include DTCs with Chile, South Korea, Canada, India, México, Portugal, Czech Republic, and Switzerland.

The tax treaty network is limited and the country lacks DTCs with some of its main trading partners, e.g. United States and Venezuela. For a number of years the shortage of tax treaties was compensated with diverse tax incentives to attract foreign investment, domestic measures to avoid double taxation and the so called contracts for legal stability. These agreements between the State and individuals/entities were intended to freeze new tax law regimes or interpretations making the tax situation adverse for the taxpayer, over a period of 20 years. The taxpayer could apply new provisions beneficial to him. As from 2013 such agreements are no longer available. Other agreements for the mutual promotion and protection of investments expressly excluded tax provisions from its scope (e.g. the treaty with Spain, 2005).

In addition to the DTC, Colombia ratified the Multilateral Convention on Mutual Administrative Assistance in Tax Matters in 2013 and became member of the OECD Global Forum on Transparency and Exchange of Information for Tax Purposes in 2015, getting the approval of phases 1 and 2 re exchange of information. Furthermore, in 2014 entered in force the Tax Information Exchange Agreement (TIEA) between the USA and Colombia. Colombia also signed a bilateral agreement for mutual assistance with Venezuela (1998) as well as a TIEA between the Republic of Colombia and the Kingdom of the Netherlands in respect of Curaçao (2012). The later agreement however does not seem to be in force. The text of majority of the tax treaties can be reached online[5].

I.4.1. Adherence to UN or OECD MC

Although Colombia is in the process of accession to the OECD, Double Taxation Conventions do not always follow the OECD Model Tax Convention and tend to rely more on the UN Model. Important deviations of the OECD Model regard, e.g.: (a) allocation rules, (b) scope and definitions of business profits, Permanent Establishments and royalties. Colombian DTCs do not define services for treaty purposes and this may collide with internal definitions of technical assistance, technical services and the understanding of intangibles such as know-how. In general, treaties do incorporate rules regarding anti-treaty shopping.

I.4.2. Special Features commonly present on Tax Treaties

Colombia classifies as a dualist state requiring all treaties to be incorporated before they can have any domestic legal effects. Furthermore, for the treaty to enter in force a control of compliance with the Constitution by the Constitutional Court is required. Treaty override is not common in Colombia.

1.4.2.1 Scope of the tax treaties

Double Taxation Conventions on Income | |||||||

|

Scope |

||||||

Country |

Income and supplementary (capital gains) tax |

CREE |

Wealth (Patrimonio / Riqueza) |

||||

Canada |

X |

X |

X |

||||

Chile |

X |

X |

X |

||||

Corea |

X |

X |

|

||||

España |

X |

X |

X |

||||

Francia |

X |

X |

X * |

||||

India |

X |

X |

|

||||

México |

X |

X |

X |

||||

Portugal |

X |

X |

|

||||

Czech Republic |

X |

X |

|

||||

Suiza |

X |

X |

X |

||||

* Only applicable if both countries derive the tax in the same taxable year |

|||||||

Transport tax treaties | |||||||

|

taxes covered |

||||||

|

Country

|

Income and supplementary (capital gains) tax |

Solidarity income tax CREE |

Wealth Patrimonio / Riqueza

|

Trade tax ICA

|

|||

Germany |

X |

X |

X |

X |

|||

Argentina |

X |

X |

|

X |

|||

Brazil |

X |

X |

X |

X |

|||

Italy |

X |

X |

X |

X |

|||

Panama |

X |

X |

X |

|

|||

Venezuela |

X |

X |

X |

|

|||

United States |

X |

X |

|

X |

|||

1.4.2.2 Variations in the definition of permanent establishments

1.4.2.3 Variations in regard dividends

|

Taxed dividends |

no taxed dividends |

|

|

General Rule (art. 10(2)(b)) |

Special rule for companies (art. 10(2)(a)) |

|

Canada |

15% |

5% when the beneficial owner is a company which holds directly or indirectly at least 10% of the shares with right to vote of the company paying the dividends |

15% |

Chile |

7% |

0% when the beneficial owner is a company which holds directly at least 25 per cent of the capital of the company paying the dividends. |

General rule: 0% if owns at least 25% and 7% for all other cases |

Special rule 38.25% or 7%* | |||

Korea |

10% |

5% when the beneficial owner is a company, partnerships excluded, which holds directly at least 20 per cent of the capital of the company paying the dividends. |

15% |

Spain |

5% |

0% when the beneficial owner is a company which holds directly or indirectly at least 20% of the capital of the company paying the dividends. |

General rule: 0% if owns at least 25% and 5% for all other cases |

Special rule 38.25% or 5%* | |||

India |

5% |

15% |

|

Mexico |

0% |

33% |

|

Portugal |

10% |

33% |

|

Czech Republic |

15% |

5% when the beneficial owner is a company, partnerships excluded, which holds directly at least 25 per cent of the capital of the company paying the dividends. |

25% |

Switzerland |

15% |

0% when the beneficial owner is a company which holds directly or indirectly at least 20% of the capital of the company paying the dividends. |

This DTC does not make any difference between taxed and not taxed dividends |

1.4.2.4 Withholding rates applicable under tax treaties

Dividends |

Interest |

Royalties |

|

Canada |

5/15 |

5/10 |

10 |

Chile |

0/7/35 |

5/15 |

10 |

Czech Republic |

5/15/25 |

0/10 |

10 |

India |

5/15 |

0/5/10 |

10 |

Korea (South) |

5/10/15 |

0/5/10 |

10 |

Mexico |

0/33 |

5/10 |

10 |

Portugal |

10/33 |

0/10 |

10 |

Spain |

0/5/35 |

0/5/10 |

10 |

Switzerland |

0/15 |

0/5/10 |

10 |

I.4.3. Treaties Currently in Force

The following treaties are in force in Colombia:

- DTC related to income for shipping and air companies, above mentioned.

- The DTCs with Canada, Chile, the Czech Republic, India, Korea (South), Mexico, Portugal, Spain and Switzerland are in force. The treaties with France and the United Kingdom are not yet applicable.

- The Multilateral Convention on Mutual Administrative Assistance in Tax Matters

- The Tax Information Exchange Agreement (TIEA) between the USA and Colombia.

- The bilateral agreement for mutual assistance with Venezuela (1998).

- The intergovernmental agreement (IGA) for the implementation of the Foreign Account Tax Compliance Act (FATCA) with the USA.

I.5. Community Law

I.5.1. Participation in a Community/Union

Colombia is a member of the Andean Community (AC), former Andean Pact. Current Member Countries include Bolivia, Colombia, Ecuador and Peru. The authorities of the Andean Community include the Court of Justice (ACJ) and the Parliament. The ACJ has issued a number of judgments concerning the interpretations and applications of the tax measures adopted by the Community in the so call “Decisiones” (hereinafter Directives), stating the rules applicable to the income tax in cross border transactions between the AC Member Countries.

I.5.2. Rules regarding Corporate Income Taxation within the Andean Community

Directives 40 and 578 govern the CIT at the AC level. The Directive 578 of the Committee of the Cartagena Agreement provides the grounds for the taxation of intra community payments within the AC, whereas Annex II of the Decision 40 governs the relations between Member States and third Countries.

AC law relies on source as the criterion to establish the country with the right to tax the income. The Directive 578, article 3, states that all kinds of income are taxable by the Member State in which the income was generated (“fuente productora”), with few exceptions, for instance profits derived by transportation enterprises and for capital gains from ships, aircrafts, buses and other means of transportation, as well as commercial papers, shares and other securities[6]. Other member countries are expected to apply the exemption method. This also applies in the case of income from services and royalties. All income taxed in other Andean countries (having its source therein) should be considered exempt in Colombia. According to the TS, expenses incurred to obtain such exempt income are not deductible.

The “fuente productora” is not necessarily related to the place of payment, nor to the performance-taking place from a specific country. Instead, the decision refers it to: 1) the place where the activity takes place if business profits are involved, 2) the place where an intangible is used or the place where the right to use an intangible is enjoyed, 3) the place where a service is performed when dealing with personal services, 4) income derived by enterprises of professional services, technical services, technical assistance and consulting services are taxable only by the member country in whose territory the benefit of such services takes place. Unless it is proven otherwise, the Decision presumes that in the latter case the benefit takes place where the expense is imputed and recorded. (the payer’s country).

A closer look to the DTCs signed by AC Member States indicate that whilst the tax treaty policy adopted by AC law to rule the relation of its Members with third countries did not play a role, the one intended for the internal market works well.

The main features for the taxation of passive income and the taxation of services in the AC Member Countries are as follows:

Colombia |

Bolivia |

Ecuador |

Peru

|

||

|

Dividends

|

5% |

– Dividends paid to foreign companies or entities without domicile in Colombia, if the profits that are paid as dividends were taxed at the corporate level – Dividends paid to residents from profits taxed at the level of the Company. – Other cases. |

25% over 50% of the dividends from Bolivian origin (effective tax rate 12,5%) |

0% – 35% |

5% |

|

Interests

|

15% |

– General rule |

25% over 50% of the dividends from Bolivian origin (effective tax rate 12,5%) |

22% |

4,99% 30% |

|

Royalties

|

15% |

– General – Software – Movies |

25% over 50% of the dividends from Bolivian origin (effective tax rate 12,5%) |

22% |

30% |

Services rendered in Colombia |

15% |

|

|||

Technical Services |

15% |

There is no withholding tax for technical services rendered from free zones. |

25% over 50% of the dividends from Bolivian origin (effective tax rate 12,5%) |

22% |

30% |

Tax holidays |

35% |

|

35% (if the payment is received by a resident) |

30% (for interest) |

|

I.5.2.1. Dividends

AC law does not define dividends, hence domestic definitions apply. For AC purposes dividends are taxed in the country wherein the company making the distribution has its domicile whereas they are not taxable in the member country where the dividends are received by the receiving company or investor, or upon distribution to the shareholders (article 10)[7].

I.5.2.2. Interest

Interest and other financial interests are taxable in the Member Country where the payment is imputed and recorded, in other terms, the member state where the debtor is located has the right to tax. For instance, in application of this allocation rule DIAN concluded that interests received by a Colombian company from a person located in another member state will be treated as except income (Concept 32229 of May 18, 2002). Interest is defined for AC purposes as income of any nature, including financial returns on loans, deposits and fund raising made by private financial institutions, with or without a mortgage guarantee, or the right to participate in the debtor’s profits, income from public funds (bonds issued by public entities) and bonds or obligations, including premiums and prizes related to such securities. Default penalties are not considered interest.

I.5.2.3. Royalties

Under Directives 578 and 40, AC Member States are obliged to tax royalty payments on a source basis. Apart from that, subject to the provisions of AC law, the Member States are competent to define the tax regime applicable to intangible technological contributions that are not capital contributions. The level of taxation varies depending on the country, but there is no possibility for tax exemption of royalty payments. The effective income tax rates for royalty payments range between 12.5% and 33% depending on the country.

One of the most controversial issues concerning AC law regards the allocation rule of royalty payments in the old conflict source vs residence[8]. This topic has not suffered any change under the Directive 578,[9] compared to the Directive 40. It seems that AC law followed the recommendation made by legal scholars in the session of the ILADT in Montevideo in 1996, proposing to follow taxation at source in every integration zone,[10] in order to avoid distortions, eliminate double taxation and simplify the tax systems.[11] A similar criterion was proposed by the Latina American Institute of Tax Law (ILADT) for its Model Tax Convention in 2010[12].

Annex II of Decision 40 rules the relations between AC Member States and third countries. In this case, AC Member States shall also follow the principle of taxation at source.[13] It applies to payments of royalties, services, professional services and technical assistance.[14]

I.5.3. Jurisprudence regarding Corporate Income Taxation within the Andean Community

The Andean Court of Justice (ACJ) has issued a number of decisions on cases related to the application of Andean Community (AC) law. Some of the most relevant are:

I.5.3.1. Business profits

In application of article 7 of the Directive 40, in connection with article 4 of its annex I, the ACJ stated that any kind of income is taxable in the country in which they are obtained irrespective of the domicile or nationality of the person who obtains it. As to the Court this as a consequence of the source taxation principle in force in the AC[15].

I.5.3.2. Services, technical services, technical assistance and consultancy

In application of article 14 of the Directive 578, the ACJ concluded that profits related to services, technical services, technical assistance and consultancy are taxed in the country where the payment is booked and registered, considering this as the country where the benefit of the services takes place. The Court points this is an exception to the source tax principle governing AC law[16].

I.5.3.3. Dividends

In a request of prejudicial interpretation, the ACJ clarified that article 11 of the Directive 40 does not indicate whether dividends should have been booked or effectively paid. As to the ACJ this issue needs to be solved according to the domestic law of the Member States[17].

I.5.3.4. Pensions

The ACJ concluded that in application of articles 8 and 9 of the Directive 583 (concerning Social security within the AC), related to the avoidance of double taxation of pensions, whenever a worker made its pension payments in its country of origin and also to the country in which he rendered services or worked, he is allowed to add the contributions made in the country of work to his country of origin. This approach would prevent losing the pension benefits or its decrease as a consequence of the migration[18].

I.5.3.5. Wealth tax

In a request of prejudicial interpretation of article 17 of the Directive 578, the ACJ concluded that such article involves a switch over clause given the purpose of the Directive to avoid double taxation and tax evasion. According to the Court the taxation of wealth (patrimonio) corresponds to the Member country in which such patrimony is located as long as that country taxes it. If that country does not tax it, the other Member state in which the taxable person is located could tax it if the wealth is subject to taxation therein[19].

I.5.3.6. Broadcasting Services

One of the landmark decisions taken in application of the Decision 40 by the State Council (SC), the maximum tribunal on tax matters in Colombia, regards the conclusion that payments derived from satellite broadcasting into Colombia are not of Colombian source and therefore not subject to a withholding tax in Colombia. The SC argued that payments made by the local operator to a foreign company are for a service related to the connection or access to the satellite located outside the national geostationary orbit. As to the SC, the income belongs to the country of domicile of the foreign broadcaster originating and sending the signal to the satellite. The SC believes that such a process takes place abroad and therefore it cannot be subject to withholding taxes in Colombia [20].

I.6. Influence of BEPS Action Plan on the Country

I.6.1. Adoption of rules in line with BEPS Reports

A number of provisions implement some actions of the BEPS reports:

I.6.1.1. Action 1

VAT is imposed on services rendered from abroad, at the place of use or consumption of the services as well as on the sale or license of intangibles related to industrial property.

I.6.1.2. Action 3

Colombia enacted CFC rules by law 1819, 2016.

I.6.1.3. Action 8, 9, 10

The transfer pricing regime includes now the Value creation criteria.

I.6.1.4. Action 13

Country by country reporting (as from 2016) concerning: 1) information related to the global allocation of revenues and taxes paid by MNE groups residents in Colombia with branches or subsidiaries abroad that are obliged to present consolidated financial statements and provided that their revenues are higher than aprox. COP2.4 billions, or 2) residents appointed as reporting entities by the foreign controlling entity.

Master file. Taxpayers are required to submit a master file with the relevant information of the multinational group, as well as a local file with the information related to each kind of transaction making evident the compliance with the transfer pricing rules.

The comparable uncontrolled price method is nowadays considered as the most appropriate method for raw materials and commodities.

In addition to the above, similar to the OECD approach, Colombian Tax Law no longer refers to the term tax havens, instead the term non-cooperative jurisdictions is in use. The law sets a number of criteria for the definition of such jurisdictions by future regulations.

I.6.2. Participation in Multilateral Instrument

Colombia is a signatory party of the MLI. DTC covered by the MLI include Canada, Chile, Czech Republic, Spain, France, India, Korea, Mexico, Portugal, Switzerland. Colombia introduced a number of reservations, the following amongst other:

- The right not to apply article 3 (transparent entities).

- Pursuant to Article 7(17)(a) of the Convention, whilst Colombia accepts the application of Article 7(1) alone as an interim measure, it intends where possible to adopt a limitation on benefits provision, in addition to or in replacement of Article 7(1), through bilateral negotiation.

- Pursuant to Article 7(17)(c) of the Convention, Colombia hereby chooses to apply the Simplified Limitation on Benefits Provision pursuant to Article 7(6).

- Pursuant to Article 10(5)(a) of the Convention, Colombia reserves the right for the entirety of Article 10 not to apply to its covered tax agreements the anti-abuse rule for permanent establishments situated in third jurisdictions.

I.7. Jurisprudence

Case law helps to illustrate that source rules are applied in an unexpected but quiet convenient way for foreign investment. A number of cases decided by the State Council between 2007 and 2015 concerning payments related to international television using satellites and communication to an automated database of a foreign company demonstrate this.

I.7.1. TV broadcasting services

In 2007, the SC addressed the issue of whether payments made to a foreign company for international television-broadcasting services into Colombia are subject to tax in Colombia. The SC did not uphold the characterization as royalties argued by the DIAN. Instead, the SC considered that payments for services are not subject to withholding tax in Colombia. In the SC view, the foreign broadcaster company and its local customer have different functions. The foreign company broadcast and rebroadcast the signal to a satellite. The local company connects to the satellite to get the signal in order to render the television service within Colombia. Therefore, payments to the foreign company are for the access to the satellite and not for rendering broadcasting services within Colombia.

According to the above mentioned, the fact that the foot print of the beam touches Colombia and the user of the signal is also located within the country are not enough reasons to sustain that the service is rendered in Colombia [21]. As a consequence, and in application of articles 406, 12 and 24 TS, the income is not considered of Colombian source and it is not subject to withholding tax [22]. This Court decision repeats as a pattern in a number of similar cases until 2015[23].

I.7.2. Income from employment

Income derived by a foreign individual rendering services in Colombia is deemed to be of Colombian sources irrespective of the existence of an employment contract with a foreign Enterprise.

I.7.3. Communication services, databases

A Colombian company (X) made payments to companies in Spain (S) and Uruguay (U) for telecommunication services required for performing its own business activity of making tourist reservations. The services allowed X to access and work on an automated database owned by a German company. However, thetwo foreign companies had outsourced the supply of the telecom service to another Colombian company (TC) and hence were contractually required to instantly forward the payment received from X to TC. X did not apply WHT in Colombia, arguing that another Colombian company (TC) was the ultimate beneficiary of the payment, and hence no WHT was due. X claimed the payment could not be considered income in the hands of either S or U because it did not accrue to them.

As to the SC, the failure to apply the WHT when required made the payment non-deductible. According to the Court: 1) the income was of domestic source and subject to WHT; 2) the payments were made to the foreign companies (S and U) as a consideration for the telecom service to enable the customers of the plaintiff (X) in Colombia to connect to the German database; (3) as such, the service is supplied within Colombia according to article 24 ITA; and 4) the beneficial ownership concept, or a possible reimbursement, argued by X was considered irrelevant for the application of the WHT[24].

1.8 Other taxes on business

As indicated previously, companies and entities doing business in Colombia may be subject to other direct taxes such as CREE, wealth tax and trade tax. The main features of these taxes are as follows:

Natural persons and companies involved in industrial activities, commercial activities and the provision of services.

Solidarity tax (so called CREE, in force up to 2017) |

Wealth tax |

Trade tax |

|

Taxable event |

Income that may likely increase the patrimony of taxpayers in the taxable year. |

The wealth tax is generated by the possession of wealth, whose value is equal to or greater than $1,000 million pesos. |

Industrial activities, commercial activities and services. |

Taxpayers |

National taxpayers whether individuals or legal entities. Companies and foreign entities taxpayers of the income tax on their income from national sources, obtained through branches and/or PEs in Colombia. |

Legal entities, individuals and illiquid succession who are taxpayers of the income tax. Companies and foreign entities taxpayers of the income tax on their income from national sources, obtained through branches and/or permanent |

Natural persons and companies involved in industrial activities, commercial activities and the provision of services. |

| Taxable Base |

Gross income minus returns, rebates and discounts results in net income. Net income minus costs incurred in the generation of net income and deductions results in the taxable income. |

Wealth of the person (For purposes of this tax, the concept of wealth is equivalent to the total gross assets of the taxpayer minus debts) | Annual gross income |

| Rate |

9% general tax rate A surcharge exists when the taxable base is equal or higher than $800 million pesos. For 2015 was of 5%, 2016 is of 6%, 2017 and 2018 will be of 8% and 9% respectively. |

The rates for the wealth tax are shown below. |

2-7 X 1000 for industrial activities 2-10 X 1000 for commercial activities and services |

Legal Persons Wealth tax for the year 2016 | |||

Taxable base range |

Marginal tax rate |

Tax |

|

Lower limit |

Upper limit |

||

>0 |

<2.000.000.000 |

0.15% |

(taxable Base) * 0,15% |

>=2.000.000.000 |

<3.000.000.000 |

0.25% |

((taxable Base – $ 2.000.000.000) * 0.25%) + $ 3.000.000 |

>=3.000.000.000 |

<5.000.000.000 |

0.50% |

((taxable Base – $ 3.000.000.000) * 0.50%) + $ 5.500.000 |

>=5.000.000.000 |

Onwards |

1.00% |

((taxable Base – $ 5.000.000.000) * 1.00%) + $ 15.500.000 |

Legal Persons Wealth tax for the year 2017 | |||

Taxable base range |

Marginal tax rate |

Tax |

|

Lower limit |

Upper limit |

||

>0 |

<2.000.000.000 |

0.05% |

(taxable Base) * 0,05% |

>=2.000.000.000 |

<3.000.000.000 |

0.10% |

((taxable Base – $ 2.000.000.000) * 0,10%) + $ 1.000.000 |

>=3.000.000.000 |

<5.000.000.000 |

0.20% |

((taxable Base – $ 3.000.000.000) * 0.20%) + $ 2.000.000 |

>=5.000.000.000 |

Onwards |

0.40% |

((taxable Base – $ 5.000.000.000) * 0.40%) + $ 6.000.000 |

Natural Persons Wealth tax for the year 2015, 2016, 2017 and 2018 | |||

Taxable base range |

Marginal tax rate |

Tax |

|

Lower limit |

Upper limit |

||

>0 |

<2.000.000.000 |

0.125% |

(taxable Base) * 0,125% |

>=2.000.000.000 |

<3.000.000.000 |

0.35% |

((taxable Base – $ 2.000.000.000) * 0.35%) + $2.500.000 |

>=3.000.000.000 |

<5.000.000.000 |

0.75% |

((taxable Base – $ 3.000.000.000) * 0.75%) + $ 6.000.000 |

>=5.000.000.000 |

Onwards |

1.15% |

((taxable Base – $ 5.000.000.000) * 1.15%) + $ 21.000.000 |

- Special acknowledgements are due to the Maastricht Centre for Taxation and to the Max Planck Institute for Tax Law and Public Finance for the time and resources made available for this report to Dr. Esperanza Buitrago. Also to PWC Colombia for the complementary access to the Tax Statute online.↵

- The laws on national taxes and tax procedures are compiled in the so-called TS (Decree 624/1989, its addendums and reforms). This Statute compiles the regulations of the taxes administered by DIAN: income tax, CREE, wealth tax, withholding taxes, VAT, GMF.↵

- Other incentives in force in the Free Trade Zones include exemptions of VAT and custom duties.↵

- Although foreign companies conducting regular business in Colombia are statutorily required to set up a local branch, they are subject to income tax only on their Colombian-source income.↵

- See http://www.dian.gov.co/contenidos/normas/convenios.html↵

- AC Decisión 578, “Régimen para evitar la doble tributación y prevenir la evasión fiscal,” may 4, 2004, Official Journal nº 1063, available at http://www.comunidadandina.org, article 3, last accessed on 1 August 2016.↵

- In this vein see , DIAN Concept 44634 of May 6, 2008.↵

- Criticism regards the repetition of domestic law. In practice AC Member States started negotiating DTCs with third countries quiet lately. Furthermore, basically none followed the AC Model for negotiation with third states.↵

- Decisión 578, Régimen para evitar la doble tributación y prevenir la evasión fiscal, en: Gaceta Oficial del Acuerdo de Cartagena, nº. 1063, 2004 http://www.comunidadandina.org/normativa/dec/D578.htm, article 9, last accessed on 1 August 2016.↵

- The most known in Latin America are CARICOM, MERCOSUR and the Andean Community.↵

- The Recommendation is available at: http://www.iladt.org/documentos/detalle_doc.asp?id=380, 3rd recommendation, last accessed on 1 August 2017.↵

- Article 9 Model Tax Convention for Latin America, as presented in the “XXV Jornadas Latinoamericanas de Derecho Tributario”, Cartagena de Indias, February, 2010.↵

- In the so called «producing source», see, Decisión 40: Aprobación del Convenio para evitar la doble tributación entre los Países Miembros y del Convenio Tipo para la celebración de acuerdos sobre doble tributación entre los Países Miembros y otros Estados ajenos a la Subregión, November 8 to 16, 1971, available at http://www.comunidadandina.org, last accessed on 1 August 2017.↵

- According to the MC approved by the Decision 40, ibid.↵

- ACJ, case 125-IP-2010.↵

- ACJ, case 37-IP-2011 y 63-IP-2011.↵

- ACJ, case 43-IP-2013.↵

- ACJ, case 100-IP-2011.↵

- ACJ, cases 171-IP-2013, 184-IP-2013, 15-IP-2014, 230-IP-2013, 111-IP-2014.↵

- SC, Judgment of July 12, 2007, fn. 15440.↵

- SC, Judgments of June 14 2007, fn. 15686; October 10, 2007, fn. 15616, 15865, 15909, 15912.↵

- SC, Judgements of August 2, 2007, refs. 15635, 15688, 15903,and February 2, 2008 ref. 16444. SC, decisions of October 3, 2007, ref. 15689. SC, decisions of October 10, 2007, refs. 15687, 15795, 15909.↵

- SC, Judgements 020544 of 2015, 017795 of 2012, 018402 of 2012, 018561 of 2012, 017252 of 2011, 016616 of 09 016401 of 2009, 015787 of 2007, 015688 of 2007. ↵

- SC judgment, of 11 December 2008, fn. 15968.↵